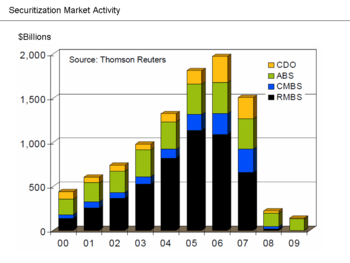

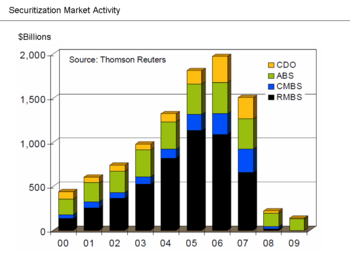

The more unicorn bubble chatter I hear, the more I think about the 2007 financial crisis and about the mispricing of risk that happened then. At the root of all the bad stuff that occurred was the severe mispricing of mortgage backed securities (MBS) and collateralized debt obligations (CDOs). Loans were pooled into portfolios and then those portfolios were sold off based on tranches of risk. These derivative securities are very complicated and the big three ratings agencies (S&P, Moody’s, Fitch) were providing favorable ratings for them at the time. Everyone went along with the ride until the market wised up. At that moment, they became unsellable “toxic assets”.

“By the end of 2009, over half of the CDOs by value issued at the end of the housing bubble (from 2005-2007) that rating agencies gave their highest “triple-A” rating to, were “impaired”—that is either written-down to “junk” or suffered a “principal loss” (i.e. not only had they not paid interest but investors would not get back some of the principal they invested).” – Wikipedia

To give you the severity of the mispricing:

“Rating agencies lowered the credit ratings on $1.9 trillion in mortgage backed securities from the third fiscal quarter (1 July – 30 September) of 2007 to the second quarter (1 April – 30 June) of 2008.” – Wikipedia

So why is this relevant today?

Because it prompts this question: Is there potential mispricing happening in the current tech boom? Here’s a stab at one answer: It’s right in front of the us on the cap tables of unicorns.

Here’s a growth stage fundraise example to illustrate how current valuations happen:

Company A growth round fundraise: $250 million

Shares sold: 10 million

Price per share: $25

Market Capitalization:

Congrats, we just made a unicorn.

If billion dollar valuations have proliferated because investors are increasingly more comfortable with them as long as they get generous downside protection, then the value of that protection has to come from somewhere. It doesn’t appear out of thin air.

That additional downside protection in the form of things such as liquidation preferences and ratchets can negatively affect the other shareholders in any exit scenario that isn’t good to great. Common shareholders have it the worst because they are at the bottom of the totem pole. In other words, the higher share price paid in later stage growth rounds should be partially offset by a decrease in price per share of the earlier classes of stock.

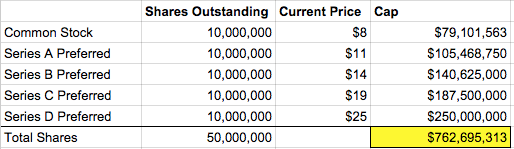

The standard method of calculating market capitalization “breaks” because not all shares are the same. Shares of Series D Preferred should be more valuable than shares of Common, Series A, B, or C.

Instead of the market capitalization calculated above, a “truer” valuation would look something like this, where the price per shares for each class should be discounted relative to the latest round:

Company A example valuation using difference prices per class of stock:

You can see this sort of exercise knocks off a lot from these valuations. If the rise of unicorn valuations are partly explained by the tradeoff of more onerous liquidation preferences and other terms being piled into the later rounds, logic says that the earlier rounds should be discounted relative to the price paid in this round.

Anyways, this is one area where the traditional accounting methods fail to tell the complete story of what’s happening these days in the growth stages of venture capital.

Is this evidence of dangerous bubbles in formation? In and of itself, no, but I’ll leave that open for you all to discuss.

Yep. I have been saying this for the last 6 months, the “billion dollar private round” is closer to $300-$500 million in a public company. Its honestly like a convertible note with a CAP of the current valuation. Which is fine if everyone understands it, but the liquidation preferences and anti-dilution rachet terms can misalign incentives in many cases I think. Very good article. And I also love the comparison to securitized debt offerings but people kept saying they would blow up, yet they got bigget and bigger until they finally crashed. Just like the current VC bubble. No doubt these companies have some actual value (unlike often was the case in 99-2000), but many times it is only say half of what they raise money from. In your example here, if a company ends up sellng for $500 million common could easily end up with NOTHING. Will be a shit show in a few years for many.

LikeLike

very interesting. a lot of times I think the general public (investor included) get so hang up on the “unicorn” status rather digging into the essence of the business. It’s somewhat silly and it’s somewhat lazy. To an extreme degree, we can write the price as high as we want (mispricing) but when reality hits, that’s the time market correction comes. We seem to live in a time that micro-startup is highly correlated with the macro economy – yet nobody want to publicly acknowledge that yet..

LikeLike

Great post, thanks! You’ve hit the nail on the head here. The secondary market is picking off a lot of people that take the valuation at face value. Sure, some get the general sense that common stock loses some downside protection and deserves a discount… but most are undervaluing the importance of this. The net “valuation” of a company should be based on the aggregate “expected value” of all shareholders… when considering the probability distribution of all outcomes. Because common stock holders (and potentially early investors) get diminished payouts in low exit scenarios, their expected $ value is less (not $1Bn simply because the last investment seems to imply it). Another way to think of the latest big $ fundraise is that it is a risk reversal (collar) where the big VC is buying a call at the strike price of the implied valuation and selling a put at the strike price of the net $ invested (or aggregate $ invested to date) if the terms are pari pasu. This is “significantly” less risky than buying stock at an implied valuation of $1Bn (in the public market, for example). Perhaps because companies w/ this kind of cash burn through it so quickly the value of the protection isn’t as great as it sounds (meaning binary outcomes are most likely vs low exits) but still it is much less risky. That’s where the control provisions come in which allow the VC to force a low exit if necessary to preserve their investment.

LikeLike