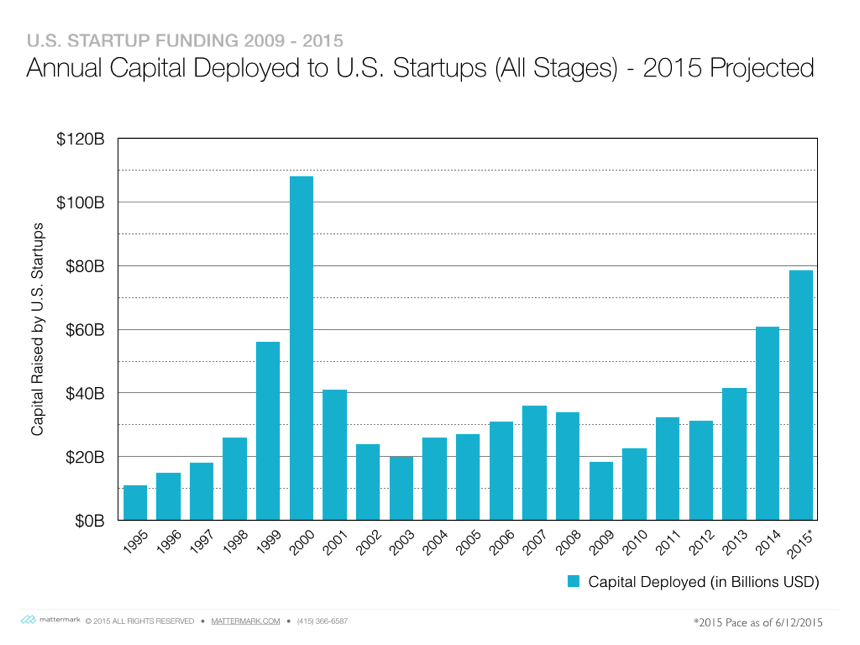

In a report recently released from Mattermark, it is indicated that investment in startups from 2014 to probable year-end 2015 will eclipse all prior years, except for 2000. Now, ‘Unicorns’ are all the rage, leading many VC firms to raise bigger funds to target larger and later stage investments. But in the world of Venture Capital, bigger is not always better.

A 2012 study by the Kaufman Foundation noted that in the years between 1997 and 2009, “only four of thirty venture capital funds with committed capital of more than $400 million delivered returns better than those available from a publicly traded small cap common stock index.” The solution, they propose, is to invest in smaller funds. In the study, Kaufman provides a number of reasons for this proposed realignment of investment allocations, the most notable being that smaller funds make their money from fund performance whereas larger funds tend to make money via fees. This pay-for-performance model makes sense intuitively, but is also far from a complete understanding of what is actually happening within the Venture Capital space.

Let’s try to break it down:

Smaller Funds have to return less capital

When a typical LP investor contributes to a late stage VC fund, they are probably doing so with an expectation to make three to five times their investment in total returns. On a $500 million fund, this means investors are likely targeting $1.5 billion – $2.5 billion in distributions at the end of the fund’s life. There’s a lot that has to go right in order to accumulate that much cash.

Small Funds don’t compete in the run-up in valuations

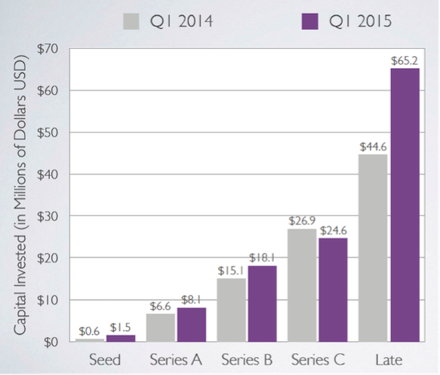

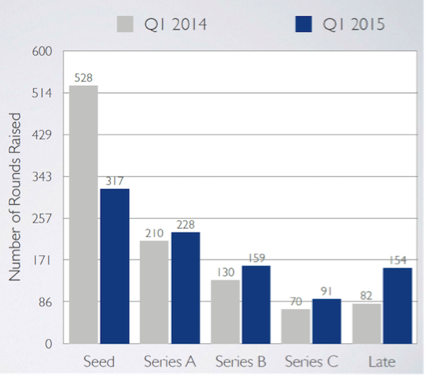

In the above case, the firm cannot realistically get all their money out the door by writing checks in $1 million increments; their ability to source enough quality deal flow and their ability to effectively monitor existing investments doesn’t scale that easily. They end up making large bets on relatively fewer later stage companies, effectively increasing their unsystematic risk which investment theory says they should diversify away. Compare the two charts below to see that Seed Investors make more investments but at very low average check sizes. This improves their risk return profile since they’re less reliant on one big winner.

Average Deal Size by Stage vs. Deal Volume

You can clearly see above that in later rounds, relatively fewer numbers of deals are getting the majority of the funds. Jason Lemkin at SaaStr estimates as much as “75% of invested capital [is] trapped in private Unicorns,” indicating investors are increasingly driving up valuations of promising later stage rounds which Small Funds simply don’t get involved in.

Smaller Funds are company builders, not just company backers

Investing in a $1 billion Unicorn means investing in a company that is already performing well, firing on all cylinders and looking to scale quickly. In contrast, investing in a $10 million company means investing in a company that is looking to make one of its first few hires, even its first sales-person, which implies they’re preparing for, but haven’t actually experienced yet, a product-market-fit. In both cases, the investor is providing capital as a value-add, but in earlier stage investing – where Small Funds predominate – the investors are often also adding much needed outside support of a more intangible nature. Oftentimes, this comes in the form of the first outside board member, able to provide much needed guidance for best-practices to technical founders with minimal business experience, or plugging the startup into a larger network full of future investors, potential advisors and even customers – all of which the startup may have failed without.

Big funds may also provide these services – a16z is famous for it – but on the whole, they are more focused on getting dollars out the door rather than nurturing budding entrepreneurs through their growing pains and company pivots. By the time a smaller fund has shepherded a company through these early stages, they have effectively helped de-risk the investment, thereby making it an attractive target to a larger fund in a much more sizable subsequent round of financing. As an existing investor, Smaller Funds can participate in these follow-on rounds which helps improve Small Fund returns by concentrating capital in their all-stars. By doing this, Small Funds magnify the impact of outperformers on the fund’s overall performance in a way less available to Large Funds, who are participating in in the last few rounds of financing prior to an IPO or eventual sale.

Early investing is not without risks

We would be remiss if we didn’t point out the other side of the coin here. Investing in unproven companies means you are investing without the benefit of past performance and the failure rate among early stage companies is notoriously high. Furthermore the risk of dilution by inflated rounds of financing in Series A and beyond is something investors must be very cognizant of and should take steps to insulate themselves against this risk. Doubling down on winners is one of many ways to do this and many early stage investors would be wise to allocate a large proportion of their fund to follow-on investments. With all that said, investing in early stage companies can provide better cash-on-cash returns, provided you have the stomach for it.